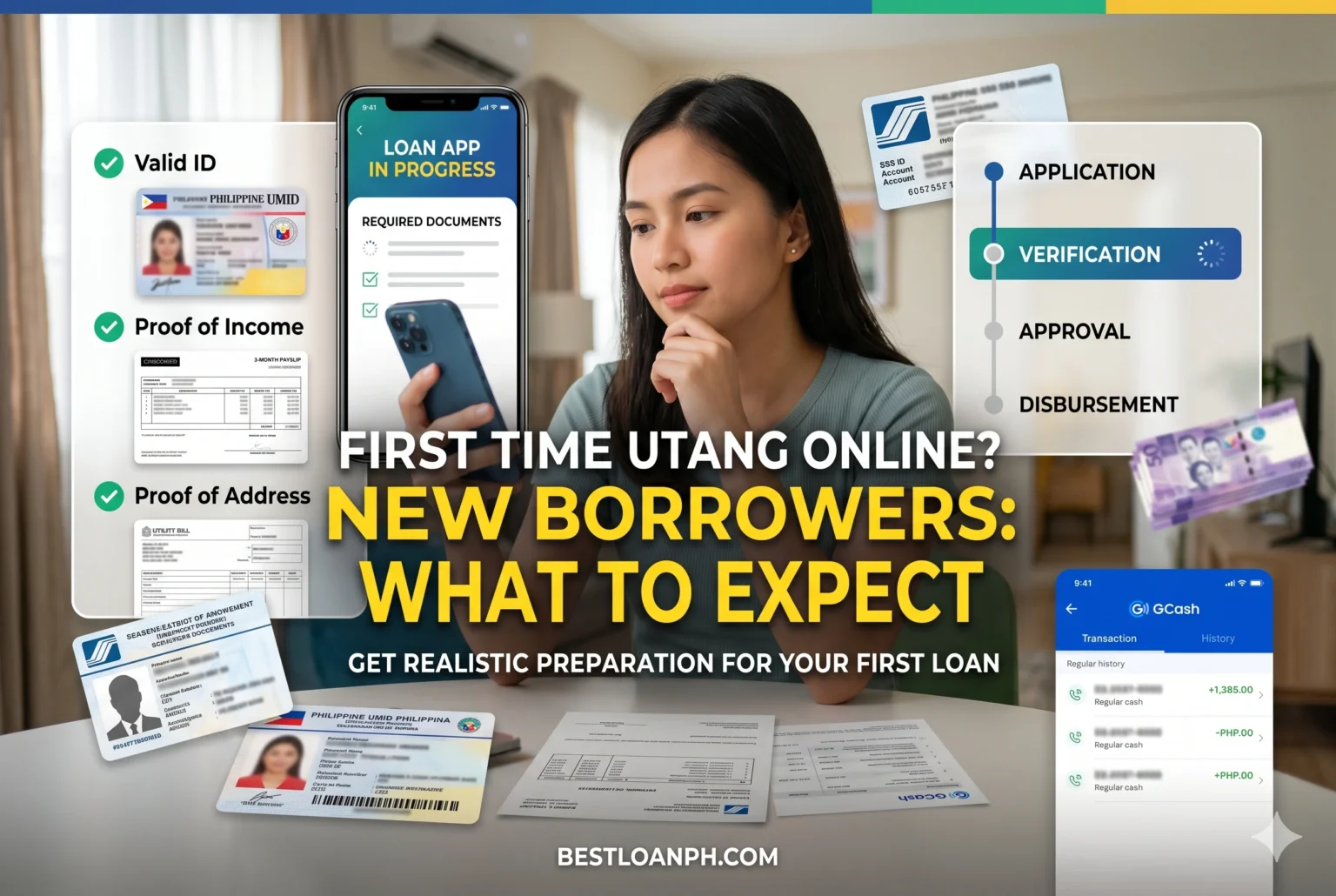

Applying for an online loan for the first time can feel intimidating, especially if you have never borrowed through a mobile lending app before. Many Filipinos worry about rejection, embarrassment, hidden checks, or whether one valid ID is enough. The good news is that first-time approval is possible even without previous loan history – but digital lenders evaluate trust differently from traditional banks. Instead of only checking salary or collateral, many apps analyze identity consistency, mobile behavior, selfie verification, device patterns, repayment risk signals, and account authenticity.

Summary

First time utang online applications are commonly approved when borrowers submit consistent identity details, stable mobile numbers, valid IDs, and verifiable e-wallet or bank information. Philippine lending apps often use selfie verification systems, OTP checks, device fingerprinting, and behavioral trust scoring to reduce fraud risk. Many first-time borrowers are rejected not because they are poor, but because their information appears inconsistent, rushed, or suspicious. Applying to too many apps at once can also reduce approval confidence. Beginners improve approval chances by preparing accurate personal data, maintaining one active SIM and device, using legitimate income details, and borrowing only manageable amounts from SEC-registered lenders.

Why First-Time Borrowers Feel Nervous About Utang Online 📱

For many users in the Philippines, the first online loan application happens during financial pressure:

- Waiting for the next payday

- Covering transportation expenses

- Paying utility bills

- Supporting family emergencies

- Handling delayed freelance income

- Recovering from short-term cash shortages

Unlike bank loans, app-based lending feels more immediate. Approval notifications arrive quickly. Some apps request selfie verification, contacts access, SMS permissions, or e-wallet linking within minutes. That speed creates anxiety for beginners who do not fully know what lenders are evaluating behind the screen.

A common fear among new borrowers is:

“What if I get rejected immediately?”

In practice, rejection is normal in digital lending ecosystems. Even legitimate borrowers can fail initial screening if the system cannot confidently verify identity or repayment reliability.

That does not automatically mean the borrower is “bad.” It often means the system lacks enough confidence signals.

What Lenders Actually Check First for New Applicants

Most first-time borrowers assume approval depends only on salary. Modern Philippine fintech lenders evaluate far more than monthly income.

Identity Consistency Matters More Than Many Beginners Realize

Digital lenders prioritize identity confidence because online fraud remains a major risk across Southeast Asian lending markets.

Before approval, many apps compare:

- Full legal name

- Birthday consistency

- Mobile number ownership

- Device history

- Selfie verification match

- Valid ID authenticity

- E-wallet account details

- GPS or location patterns

- Typing behavior in some systems

If your ID says “Juan Dela Cruz” but your e-wallet uses a nickname and your application uses incomplete spelling, automated systems may flag the application for mismatch review.

This is why many beginners fail even when they have income.

Device Fingerprinting Quietly Affects Approval

Many Philippine lending apps use device fingerprinting systems to detect suspicious activity.

These systems may evaluate:

- How many accounts were created on the device

- Whether the phone appears rooted or modified

- SIM switching frequency

- Emulator usage

- VPN behavior

- Multiple applications from one device

Borrowers sometimes unknowingly hurt approval chances by borrowing phones from friends or applying through internet cafés.

A clean and consistent personal device generally creates stronger trust signals.

Why First Applications Commonly Fail ❌

Rejection is often connected to behavioral patterns rather than income alone.

Applying to Too Many Apps at the Same Time

One of the most common beginner mistakes is mass-applying across multiple lending platforms within a few hours.

New borrowers often panic and think:

“Maybe one of them will approve me.”

However, many fintech systems monitor rapid application activity. Multiple simultaneous attempts can appear desperate or fraudulent.

This behavior may reduce borrower trust scoring because:

- It suggests possible over-borrowing risk

- It indicates repayment pressure

- It resembles fraud-ring behavior

- It lowers confidence in repayment stability

Submitting fewer, more accurate applications is usually safer.

Incomplete or Rushed Applications

Beginners sometimes rush through onboarding screens without reviewing details carefully.

Common issues include:

| Mistake | Possible Result |

|---|---|

| Blurry ID photo | Verification failure |

| Poor selfie lighting | Facial mismatch |

| Wrong birthdate | Identity inconsistency |

| Disposable SIM number | Low trust score |

| Inconsistent income details | Risk flag |

| Fake references | Manual rejection |

Many approvals are automated. Small inconsistencies can immediately lower approval probability.

Unrealistic Loan Amount Requests

A first-time borrower requesting a very high amount may appear risky.

Most online lenders gradually build trust through smaller starting limits.

For example:

- First loan: small amount

- Successful repayment: higher confidence

- Repeat repayment success: larger future eligibility

Borrowers with no digital lending history are usually safer requesting modest amounts initially.

Can First-Time Borrowers Really Get Approved?

Yes. Many first-time borrowers in the Philippines successfully receive online loans every day.

But approval depends heavily on whether the platform believes the borrower is:

- Real

- Reachable

- Financially stable enough

- Consistent across records

- Likely to repay on time

Digital lending systems are designed to reduce fraud and default risk quickly.

That means beginners can still qualify even without:

- Credit cards

- Previous bank loans

- Formal bank relationships

Especially now that fintech lenders increasingly evaluate:

- E-wallet activity

- Payroll consistency

- Gig work patterns

- Freelance cash flow

- Digital identity behavior

- Stable mobile usage

This has expanded access for younger workers and first-time earners.

Young Workers Often Face Different Approval Behavior

A fresh employee receiving their first salary may still qualify for online lending, but lenders usually apply tighter caution.

Age and Employment Stability Influence Risk Models

Some lending systems view younger borrowers as higher risk because they often have:

- Short employment history

- Limited repayment records

- Frequent job changes

- Lower emergency savings

That does not mean young applicants are automatically rejected.

Instead, systems may approve:

- Lower starting limits

- Shorter repayment periods

- Smaller initial disbursements

Borrowers who repay early or on time usually improve future eligibility significantly.

Freelancers and Gig Workers Are Increasingly Accepted

Philippine digital lenders have adapted to the rise of:

- Food delivery riders

- Freelancers

- Online sellers

- Content creators

- Remote workers

- Ride-hailing drivers

Traditional payslips are no longer the only accepted proof of income.

Some platforms now evaluate:

- GCash transaction activity

- Bank inflows

- Consistent e-wallet cash movement

- Platform earnings screenshots

- Digital payment behavior

This reflects broader fintech evolution in the local lending market.

Is One Valid ID Enough? 🪪

Sometimes yes, but approval depends on the lender’s verification policy.

Why Some Apps Accept Only One ID

Certain smaller loan amounts may require:

- One government-issued ID

- Selfie verification

- Active mobile number

- E-wallet or bank account

This helps streamline onboarding for first-time users.

Why Additional Verification Is Still Common

Even if one ID is technically enough, systems may request extra proof when risk confidence is low.

Additional verification can include:

- Secondary IDs

- Employment details

- Billing information

- Video verification

- Contact references

- Social verification patterns

This is especially common when:

- The selfie is unclear

- The ID appears damaged

- The address cannot be validated

- The device has suspicious activity

Borrowers should not interpret extra verification as personal targeting. It is often automated fraud prevention logic.

For updated borrower protection reminders and SEC lending advisories, users can review official notices from Securities and Exchange Commission Philippines and consumer guidance from Bangko Sentral ng Pilipinas.

Why Apps Ask for Contacts and Permissions

This is one of the biggest emotional concerns for beginners.

Contacts Access Is Usually Part of Risk Assessment

Some digital lenders request contacts access to help assess account authenticity and fraud risk.

Historically, certain abusive lending apps misused this practice. Because of that, borrowers today are more cautious – and rightly so.

Legitimate lenders should follow Philippine privacy and data protection expectations under rules enforced by the National Privacy Commission.

Borrowers Should Still Be Careful

Before installing any lending app:

- Verify SEC registration

- Read Play Store reviews carefully

- Avoid apps with harassment complaints

- Review permission requests

- Avoid apps demanding unnecessary access

This matters because not all platforms operate with the same standards.

The safest approach is to prioritize reputable platforms with transparent policies and clear repayment disclosures.

This connects closely with broader safe online borrowing tips that help beginners avoid predatory lenders.

Borrower Trust Scoring Happens Quietly Behind the App

Most users never see the internal scoring systems evaluating them.

Modern Lending Apps Analyze Behavioral Consistency

Approval engines may evaluate:

- How quickly forms are completed

- Whether details change repeatedly

- SIM card age

- Device reliability

- Location consistency

- Previous repayment ecosystem data

- Duplicate account indicators

Some fintech companies also integrate alternative credit scoring methods using broader digital behavior signals.

This helps lenders approve borrowers who may lack formal bank credit history.

Stable Digital Behavior Builds Confidence

Strong trust signals often include:

- Long-used mobile numbers

- Consistent addresses

- Real employment information

- Active e-wallet accounts

- Genuine references

- Clean ID submissions

Borrowers trying to “look richer” by exaggerating salary details can actually create verification conflicts.

Accuracy matters more than inflation.

Why Rejection Should Not Feel Embarrassing

Many first-time borrowers take rejection personally.

In reality, automated systems reject applications for many technical reasons:

- Weak image quality

- Identity uncertainty

- Incomplete metadata

- Risk model limitations

- Temporary verification issues

- System congestion

- Fraud-prevention triggers

Even financially capable users can fail automated onboarding temporarily.

This is especially true during periods of:

- High application traffic

- Payday demand spikes

- Emergency loan surges

- Promotional campaigns

A rejection does not define your financial future.

Practical Ways Beginners Can Improve Approval Chances ✔️

Prepare Your Identity Information Before Applying

Before opening the app, prepare:

- Government-issued ID

- Stable SIM number

- Active e-wallet

- Correct employment details

- Address information

- Emergency contacts

This reduces rushed mistakes.

Use Good Lighting During Selfie Verification

Selfie verification systems compare facial details against ID images.

Common failure reasons include:

- Dark rooms

- Face masks

- Tilted camera angles

- Blurry front cameras

Simple lighting improvements can significantly help automated verification accuracy.

Avoid Multiple Same-Day Applications

Submitting many applications quickly may reduce trust scoring.

Instead:

- Choose a reputable lender

- Complete one clean application

- Wait for result feedback

- Correct issues before reapplying elsewhere

This creates healthier application behavior patterns.

Start With a Smaller Loan Request

New borrowers are often safer requesting manageable amounts first.

Smaller initial borrowing helps establish:

- Repayment history

- Platform trust

- Behavioral reliability

Future approvals may improve after successful repayment.

How Fast Online Loan Release Usually Works ⏱️

Many beginners believe approval automatically means instant cash release.

That is not always true.

Approval and Disbursement Are Different Steps

After approval, lenders may still process:

- Bank validation

- E-wallet verification

- Fraud screening

- Queue management

- Manual review

This is why some users wait longer than expected.

Borrowers curious about disbursement timing can also read more about how fast online loan release works to better understand processing expectations.

E-Wallet Verification Is Increasingly Important

Many Philippine fintech lenders now prioritize:

- GCash-linked disbursement

- Maya wallet validation

- Digital bank transfers

- OTP-secured payout confirmation

Mismatch issues between borrower name and e-wallet ownership can delay release.

Consistency across accounts matters heavily.

First-Time Borrowers Without Loan History Still Have Options

Traditional banks often rely heavily on formal credit history.

Digital lenders increasingly use alternative trust evaluation methods.

This shift has helped:

- Young professionals

- New employees

- Freelancers

- Small online sellers

- Gig workers

- Rural mobile-first users

However, fintech accessibility does not remove repayment responsibility.

Borrowers should still evaluate:

- Interest costs

- Due dates

- Penalties

- Collection policies

- Repayment ability

Before applying for any utang online philippines option, beginners should read terms carefully and avoid borrowing emotionally during panic situations.

Common Emotional Mistakes First-Time Borrowers Make

Borrowing Out of Fear Instead of Planning

Some borrowers apply late at night under pressure and skip important details.

This often leads to:

- Wrong repayment assumptions

- Missed due dates

- Unread penalties

- Over-borrowing

Slowing down before submission improves decision quality.

Feeling Forced to Accept Any Offer

Not every approved loan is a good loan.

Review carefully:

- Interest computation

- Processing fees

- Extension charges

- Collection practices

- Due date structure

Approval alone should not determine acceptance.

What Beginners Should Know About Online Loan Safety 🔒

New borrowers are often targeted by fake lenders, cloned apps, or phishing attempts.

Warning Signs of Unsafe Lending Apps

Be cautious if an app:

- Guarantees approval instantly without verification

- Requests advance payment before release

- Uses threatening language

- Has no SEC registration visibility

- Has large volumes of harassment complaints

- Requests suspicious permissions

Legitimate lenders still perform KYC verification and identity screening.

Real Verification Is Normal

Many beginners fear selfie checks or OTP verification.

But these systems are standard fintech security practices designed to reduce:

- Identity theft

- Fake applications

- Account takeovers

- Fraudulent borrowing

The key difference is whether the lender handles borrower data responsibly and transparently.

You can also review broader explanations about current utang online requirements before choosing a lending platform.

FAQs About First Time Utang Online

Can first-time borrowers get approved without credit history?

Yes. Many digital lenders evaluate identity consistency, income signals, device trust, and e-wallet behavior instead of relying only on traditional credit history.

Does age affect online loan approval?

Sometimes. Younger borrowers may receive smaller starting limits because lenders have less repayment history to evaluate. Stable employment and consistent identity data can still improve approval chances.

Why do lenders ask for selfie verification?

Selfie verification helps confirm that the borrower matches the submitted ID. This reduces identity fraud and fake account creation.

Is using multiple loan apps at once bad?

It can reduce approval confidence. Rapid applications across several apps may appear risky to automated lending systems.

Can freelancers qualify for first-time online loans?

Yes. Many lenders now consider alternative income patterns such as freelance payments, e-wallet cash flow, and digital transaction activity.

Why was my first application rejected even with income?

Rejections may happen because of blurry IDs, inconsistent details, suspicious device activity, weak verification confidence, or automated fraud checks – not only because of income level.

Conclusion

Applying for a first time utang online loan can feel stressful, especially when you do not know how digital lenders evaluate new borrowers. But approval decisions are usually based on trust signals, identity consistency, verification quality, and realistic repayment confidence – not simply whether you are wealthy or experienced.

Beginners improve their chances by applying carefully, using accurate information, maintaining stable digital accounts, and borrowing manageable amounts from legitimate lenders. Avoid panic applications, rushed submissions, and unrealistic expectations.

Online lending can be useful when handled responsibly. The safest first step is preparation, patience, and choosing platforms that respect borrower privacy, transparency, and fair repayment practices.

Last Updated: May 29, 2026 by The Nomad Finance Girl (Jaycee)